Once might be a coincidence, three times might be luck, but what about the 10th time?

Starting in the second half of 2025, some traders following Bitcoin's movements on Twitter noticed something strange. They reviewed the intraday charts from the past six months and grew increasingly suspicious: almost every day around 10 AM, just as the U.S. stock market opened and market sentiment was most active, Bitcoin would experience a sharp, clean drop, precisely erasing its earlier gains.

He posted this discovery on Twitter, and unexpectedly, the comments section exploded with others who had noticed the same thing: "I noticed it too," "It's been going on for months," "This is definitely not a coincidence."

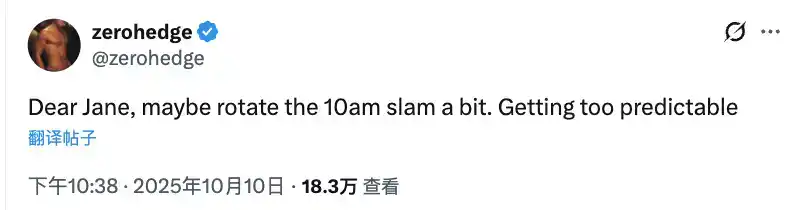

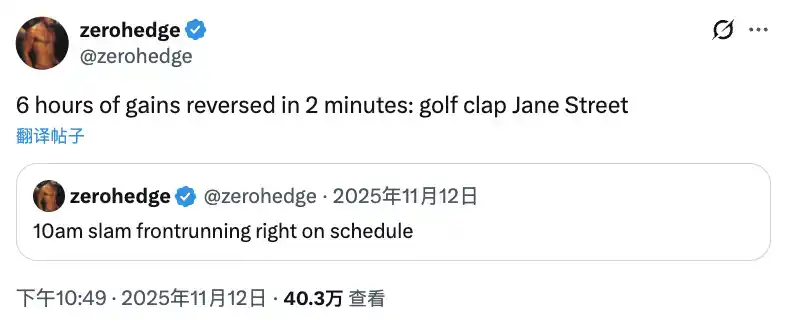

Financial media outlet ZeroHedge was even more direct, tweeting one message after another since last July, pointing the finger squarely at one of the main market makers for the spot Bitcoin ETF: Jane Street. After the 10 AM dump, Jane Street quietly accumulates, holding over $2.5 billion in BlackRock's Bitcoin ETF, IBIT.

They even gave this phenomenon a name: the "Jane 10 AM Dump Strategy." And what recently brought this rumor back into widespread circulation was a lawsuit from Terra.

An Intern Named Bryce

Recently, the bankruptcy administrator for Terraform Labs filed a lawsuit in court. The defendants are Jane Street, Jane Street's co-founder Robert Granieri, and two traders, Bryce Pratt and Michael Huang.

This is an extremely low-profile company on Wall Street. It never gives media interviews, never brags about its profits publicly, and for a long time, people outside the circle didn't even know it existed. But within the financial industry, the name Jane Street is almost universally known—it's an institution that has made tens of billions of dollars through quantitative trading and market making, with annual profit per employee unmatched anywhere else on Wall Street.

The core allegation in the lawsuit is, in essence, not complicated: on the eve of the collapse of UST (TerraUSD) in 2022, Jane Street used non-public information obtained from insiders to exit their positions early, quietly getting out unscathed before the entire $40 billion Terra ecosystem turned to dust.

And the starting point of this "insider information" trade was a young man named Bryce Pratt.

Bryce Pratt had previously interned at Terraform and later joined Jane Street. Under normal circumstances, a previous internship would be just an insignificant line on a resume. But the court complaint spends a full three pages, from page 29 to 31, describing him for one reason only: after leaving Terraform, he didn't really leave.

He created a private group chat, adding a Terraform software engineer and the head of business development. The group was named "Bryce's Secret."

The name was rather blunt, and rather bold. According to the lawsuit, the function of this group chat was to continuously funnel internal information from Terraform back to Jane Street. At the same time, Bryce also acted as a bridge, introducing Terraform's head of business development to the leader of Jane Street's "DeFi department," and the two sides began regular communications under the guise of "exploring strategic investment cooperation."

From the lawsuit's perspective, Jane Street effectively turned this communication channel into a backdoor for continuously obtaining material non-public information.

Jane and Terraform Have a Little-Known History

Rewind a bit further.

The relationship between Jane Street and Terraform didn't start with Bryce Pratt's group chat; it started earlier. In May 2021, during the first de-pegging of UST.

That time, UST briefly deviated from its dollar peg, causing panic throughout the Terra ecosystem. To stabilize the situation, Terraform Labs began contacting institutional trading partners for large-scale over-the-counter (OTC) arrangements. Jane Street was one of them.

According to the lawsuit, in this relationship, Terraform provided Jane Street with large trading allocations for UST and Luna, and at certain stages offered discounts or structural incentives in exchange for their providing support during critical moments. These terms were never disclosed to the public.

This means the relationship between the two companies was not ordinary market trading from the start, but a contractual, interest-aligned bond. It is this layer of relationship that makes the insider trading allegations harder to dismiss legally—when you have a secret agreement with the other party and simultaneously hold their non-public internal information, any trade you make appears highly unusual.

Time moved to early 2022. On the surface, the Terra ecosystem was at its peak: the Luna Foundation Guard (LFG) had just been established, absorbing reserves of Luna worth approximately $5.5 billion, and used $3 billion to purchase other assets, presenting an image of an impregnable fortress. However, beneath this glossy surface, signs of trouble were emerging: deposit sizes on the Anchor protocol began to face pressure, UST's reliance on the peg rate intensified, and the rate of LFG's reserve consumption quietly accelerated.

Not many people knew this. But Jane Street happened to be one of them.

10 Minutes Before a $40 Billion Empire Collapsed

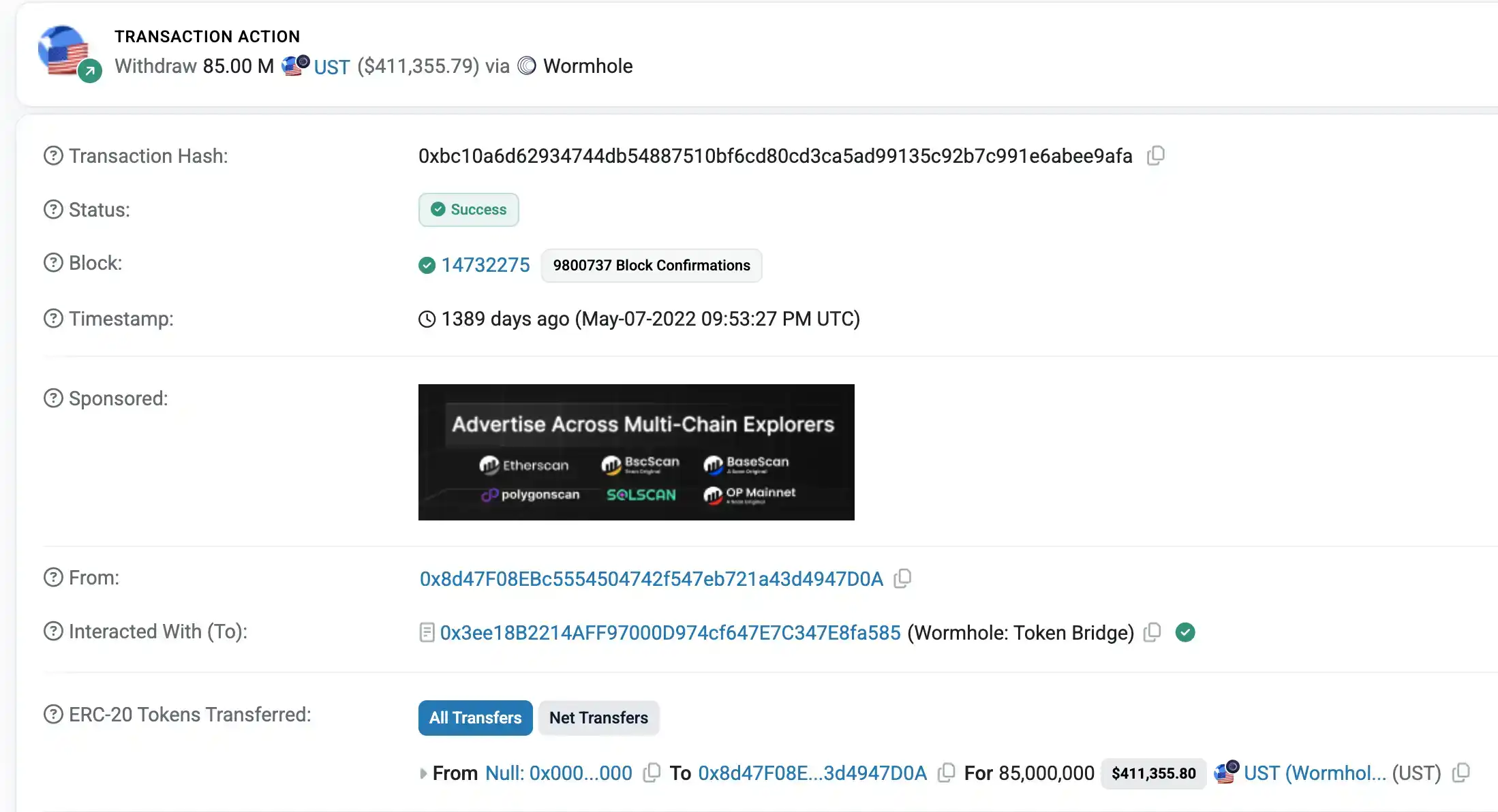

May 7, 2022, Eastern Time, 5:44 PM.

Terraform quietly withdrew 150 million TerraUSD from the Curve 3pool—a liquidity pool specifically for swapping dollar stablecoins. No announcement, no warning, no public statement.

This operation was completely unknown to the outside world at the time.

Yet, less than ten minutes after these funds were withdrawn, a wallet identified by on-chain analysts as associated with Jane Street withdrew 85 million TerraUSD from the same liquidity pool.

The lawsuit further alleges that Jane Street's unusual actions did not stop there. Before the de-pegging of UST became apparent and public panic began to spread, addresses associated with Jane Street had already systematically de-risked—large-scale selling of UST, adjusting related positions, reducing their net exposure to the Terra ecosystem to a minimum. Some specific figures are redacted in the lawsuit, usually indicating commercial confidentiality or evidence not yet public, but the fund flow trajectories tracked by on-chain analysts are sufficient to tell the story.

Meanwhile, Terraform and LFG were doing the exact opposite.

On May 7, Terraform bought over 250 million UST. On May 8, it bought another over 200 million. In the following days, cumulative purchases exceeded 1.9 billion UST, plus over 90 million Luna. As for LFG, by May 16, its UST holdings soared from about 700,000 to over 1.8 billion, an increase of over 1.7 billion; its Luna holdings surged from 1.7 million to over 222 million.

Another piece of evidence is a report published by on-chain data analysis firm Nansen on May 27, titled "On-Chain Forensics: Unraveling the Mystery of TerraUSD's Depegging." The report did not directly name Jane Street but detailed several wallets that played key roles during the de-pegging, including one later alleged to be associated with Jane Street. The report's conclusions were two-fold: first, these fund movements occurred before the market panic became apparent; second, there was a significant time gap between these operations and the publicly visible crash timeline.

Suspected Jane Street-associated address withdrew 85 million TerraUSD

The lawsuit also mentions that after the trades on May 7 were completed, Jane Street did not stop. They allegedly continued to use confidential information obtained from Jump Trading to further trade TerraUSD and amplify their gains. Jump Trading had previously secretly agreed with Terraform to intervene and support the price, ultimately profiting billions from the collapse.

In India, They Did the Same Thing

Now, attentive researchers have noticed that after Jane Street was sued by Terra, the 10 AM dumps disappeared. This seems to further confirm the rumors of the "Jane 10 AM Dump Strategy."

On the other side of the world in India, regulators had already formed their own judgment about Jane Street.

The Securities and Exchange Board of India (SEBI) issued a provisional order, 105 pages long, imposing a record fine of 48.43 billion rupees—approximately $570 million. This figure is unprecedented in Indian regulatory history, and SEBI's findings read remarkably similar to the allegations in the Terra Luna case.

SEBI believes Jane Street implemented a carefully designed "pump and dump" strategy in the Indian market.

The logic is as follows: First, use large-scale directional buy orders in the relatively illiquid spot and futures markets to artificially push the Nifty Bank Index (BANK NIFTY) up or down; after the price is pushed to the desired level, immediately execute reverse operations in the highly liquid options market, harvesting retail traders who followed the trend; finally, systematically dump the previously built spot positions, causing the index to fall back, rendering the options held by retail traders worthless, while the value of their own reverse positions soars.

SEBI's report cited a specific example: on January 17, 2024, Jane Street built a long position of approximately $67 million in just 8 minutes. Their trading volume was more than three times that of the market's second-largest participant, and this single buy order alone pushed the index up over 1%.

The regulator's wording was毫不客气 (unsparing),称 (calling) Jane Street's actions "trading to influence the price, not being guided by the price to trade," constituting a "deliberate, well-planned, sinister scheme and artifice" with the sole intention of misleading the market, particularly by exploiting the vast number of inexperienced retail participants.

Jane Street was for a long time a classic case of this narrative. The company is known for being extremely low-profile, never giving media interviews, never boasting to the outside world. It amassed astonishing wealth through quantitative trading and market making, achieving a near-mythical status within the circle. Every recruitment season, the salary figures it offers drive Wall Street's new graduates crazy, with competition as fierce as any top-tier institution.

However, starting from a certain point, the stories about this company began to become more complex.

In the Terra Luna case, it is accused of using insider information to escape early, completing its retreat while Terraform and LFG were desperately propping up the market with billions. In the Indian market, it was identified by regulators as systematically manipulating spot and derivative prices to harvest ordinary investors. Alameda Research—the core team behind FTX, which dragged the entire crypto industry into its darkest hour—had many members from Jane Street, and its founder, SBF, admitted that his market thinking framework was learned at Jane Street. Additionally, Jane Street is known for aggressively suing former employees, its维权 (rights protection/legal action) being notably vigorous even by Wall Street standards. An earlier investigative report even linked it to weapon procurement funds in a coup attempt in South Sudan, although the details remain disputed.

Information is power; information represents hierarchy.

Jane Street's "track record" seems to be more extensive than we imagined, and Jane Street's reputation has indeed taken a hit in recent years. Although the lawsuit against Jane Street has not yet reached a conclusion.

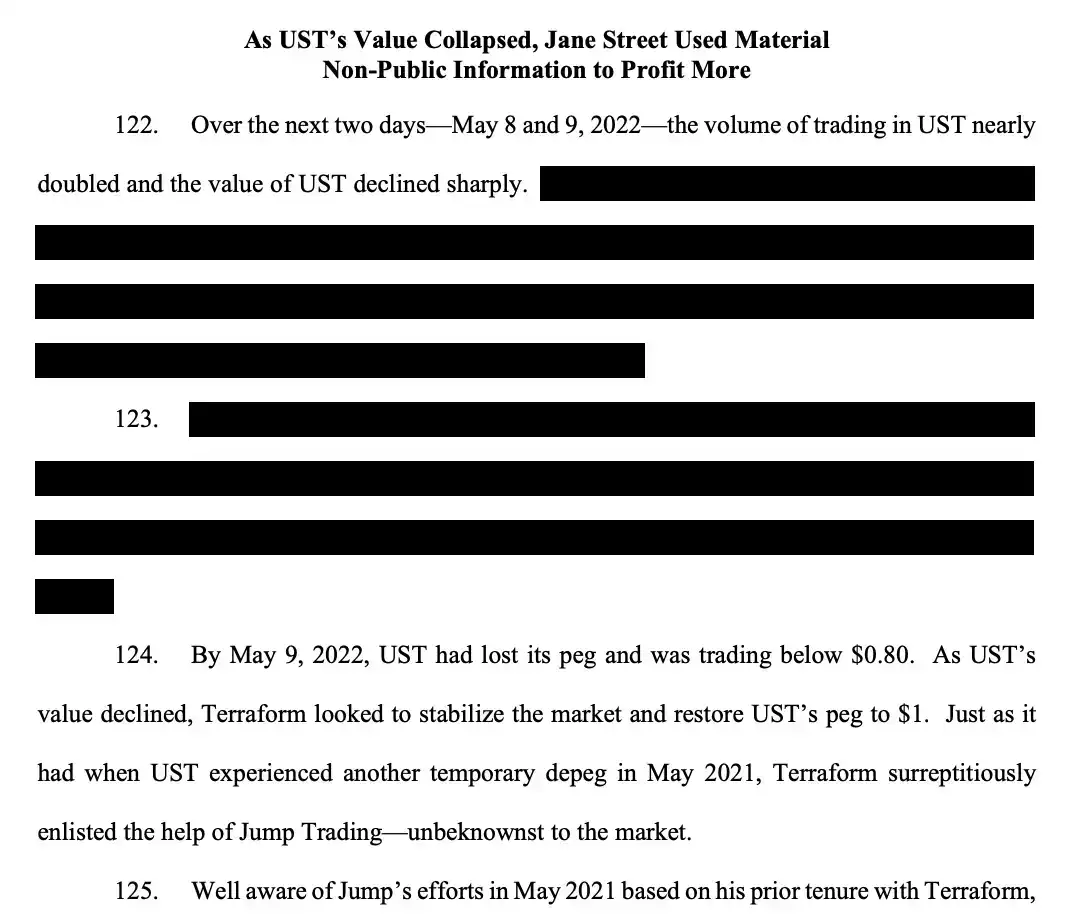

But for one company to appear in so many negative stories simultaneously, is itself a signal.